If America were to get a grade in personal finance, it would be an “F.”

According to an article in Forbes, “Two-thirds of American adults can’t pass a basic financial literacy test.” But more important than a test score is the critical state of most Americans’ finances.

- 44% of Americans can’t cover a $400 emergency without going into debt.

- 43% of student loan borrowers are behind on loan payments.

- 56% of Americans have saved less than $10,000 for retirement.

The good news is there is a solution. But first we need to understand the “why” behind this widespread financial problem. One reason is that Americans are averse to discussing finances, even with those they love. CNBC reports that 44% of Americans “would rather discuss death, religion or politics than talk about personal finance with a loved one.”

People aren’t sharing what they know, and it’s having a big impact on the younger generation. According to Annamaria Lusardi, founder and academic director of the Global Financial Literacy Excellence Center at George Washington University’s School of Business, “One in five American high school students [lack] even basic financial skills — such as the ability to interpret a pay stub to determine how much money will be deposited into their bank account or the savvy to avoid being tricked into sharing an online bank account logon.” In fact, the Federal Trade Commission reported that more Millennials lost money to financial scams than any other age bracket. This includes seniors, who are often seen as the traditional target.

“The Federal Trade Commission reported that more Millennials lost money to financial scams than any other age bracket. This includes seniors, who are often seen as the traditional target.”

Even people who are highly educated in other areas of their life can be vulnerable. High school science teacher and father of three Brian Bean worked hard to earn a good credit score. His limited teacher’s salary didn’t give him a lot of extra funds, but he wanted to be responsible with the money he did have.

Brian got involved with a financial coaching firm who said they could leverage Brian’s good credit to make financial and real estate investments that would earn him increased dividends in the future. “I was pretty naive at the time,” Brian says. “I didn’t know much about personal finance or fancy investing and the individuals seemed trustworthy, so I believed in them.” As time progressed, Brian started to notice some red flags. He started looking closer into his financial situation and realized the company had leveraged his personal credit for $1.2 million of debt. “It was basically an elaborate Ponzi scheme,” Brian says. “And I was a school teacher qualifying for food stamps. I ended up having to declare bankruptcy and start life over at 30.”

Brian’s story doesn’t end here. Keep reading to find out how he helps students avoid making the same mistake.

What About Financial Literacy Education?

It’s tough for parents to pass on financial skills they don’t have, especially if they’re averse to even bringing up the topic of money. But where does that leave the next generation? If children aren’t being taught about finances at home, are they at least learning something in school?

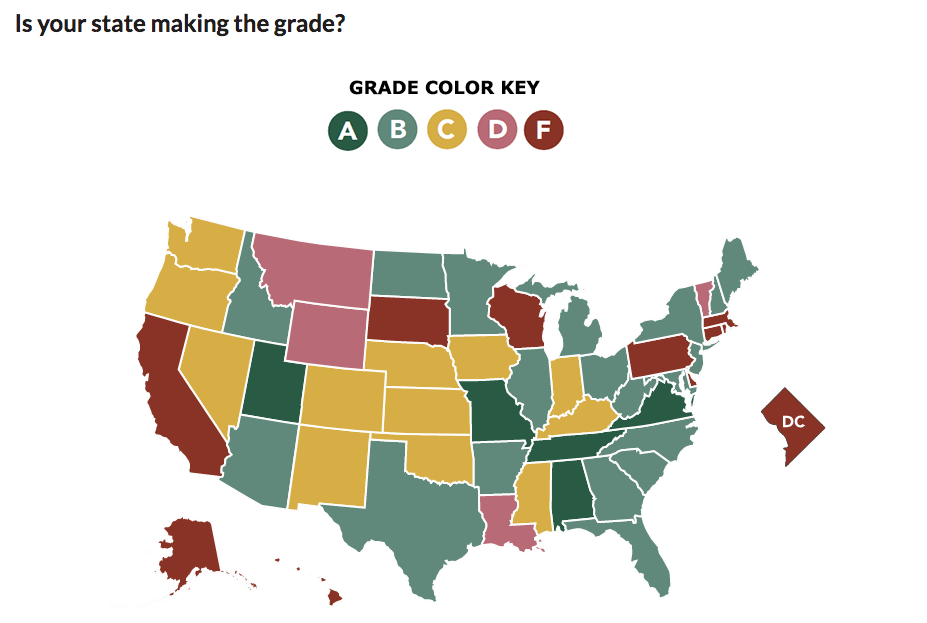

The answer is: maybe. In 2017, Champlain College released a national report card on financial literacy in high school and 27 states received a grade of “C” or lower. Nationwide, only 17 states required high schools to teach personal finance in 2018.

The irony is that many young adults actually want to learn about money management. The Financial Educators Council surveyed 1,101 young adults ages 18-24 about which high school course would benefit their lives the most. The majority said “money management” would have the most value for them after high school.

So if schools know there’s a deficiency and students are willing to learn, why do our efforts keep falling short?

In 2017, Champlain College released a national report card on financial literacy in high school and 27 states received a grade of “C” or lower. Source: Champlain College

Three Recommendations for Improving Financial Education

In an article in Bloomberg Opinion, Barry Ritholtz, founder of Ritholtz Wealth Management and former chief executive and director of equity research at FusionIQ, cited academic research that reviewed more than 200 studies and found that the lessons of financial education are “fleeting and degrade quickly without frequent use.” He then gave three possible solutions for improving the state of financial education in schools:

- Hands-on education: As Ritholtz put it, “Teaching finance is not well-served by the standard format of classroom lectures. Instead, if we want to make students proficient in budgeting, help them understand credit, and teach them about investing, a better approach would be a learning experience from real life.” He emphasizes that the “lecture-and-test” approach has been proven not to work by multiple studies.

- Repetition: Students learn from doing things over and over. If they talk about something once in school but never do it again, they won’t truly learn and retain the knowledge and skills. Ritholtz emphasizes the importance of education continuing beyond high school and into their real lives, including the financial services they use as adults.

- How to think: Memorizing and regurgitating facts has little effect on actual problem-solving skills. Ritholtz goes so far as to call it the “education equivalent of fast food” and says that a more effective method is to “let the students figure out the ideas for themselves, with the instructor as the pilot. This sort of approach leads to harder-won knowledge, which tends to be more durable.”

How One Teacher Is Putting Knowledge Into Action

Remember Brian Bean, the high school science teacher who fell victim to a Ponzi scheme and was mentioned earlier in this article? Brian’s story doesn’t end with declaring bankruptcy. He actually went back to school and got a degree in banking and finance. He also got a master’s degree in teaching methodology and developed the Real-World Classroom Teaching Model. He then created a one-of-a-kind personal finance simulation, Mimic Personal Finance, that helps students actually experience personal finance, not just learn about it.

Apply for the free trial here.

3 Pillars of the Real-World Classroom Teaching Model

Brian’s unique approach to teaching personal finance is based on three core concepts that are surprisingly similar to the recommendations given by Ritholtz.

- Realify not Gamify. Mimic Personal Finance gives students real-world consequences for their financial choices.

- Focus on the Decision-making Process. Brian created an environment where students’ choices dictate the learning experience. Through the decision-making process, students master the content and more effective learning occurs.

- No One-size-fits-all Solution: Create a Differentiated Learning Experience for Students. Students shouldn’t be taught that there is only one way to achieve and define financial success, but should be allowed to explore how effective their personal approach is so that they can recognize their strengths and weaknesses. By letting choices dictate outcomes, a differentiated learning experience is naturally created.

Free Resource for the 2019-2020 School Year

Stukent is offering 2,000 high schools the opportunity to use Mimic Personal Finance for FREE during the 2019-2020 school year. To apply for a grant, go to www.stukent.com/mimic-personal-finance.